Workplace benefits: Communication gap or translation opportunity?

Guest Contributor: Mike Dullaghan, Director of Retirement Sales Execution, Franklin Templeton

Background:

For years, the retirement industry has framed the challenge the same way: participants aren’t engaged enough. Employers need better communication. Advisors need to educate more. But the latest Voice of the American Workplace research by Franklin Templeton suggests something more nuanced—and actionable: the partnership already exists. It just needs to be activated.

Findings:

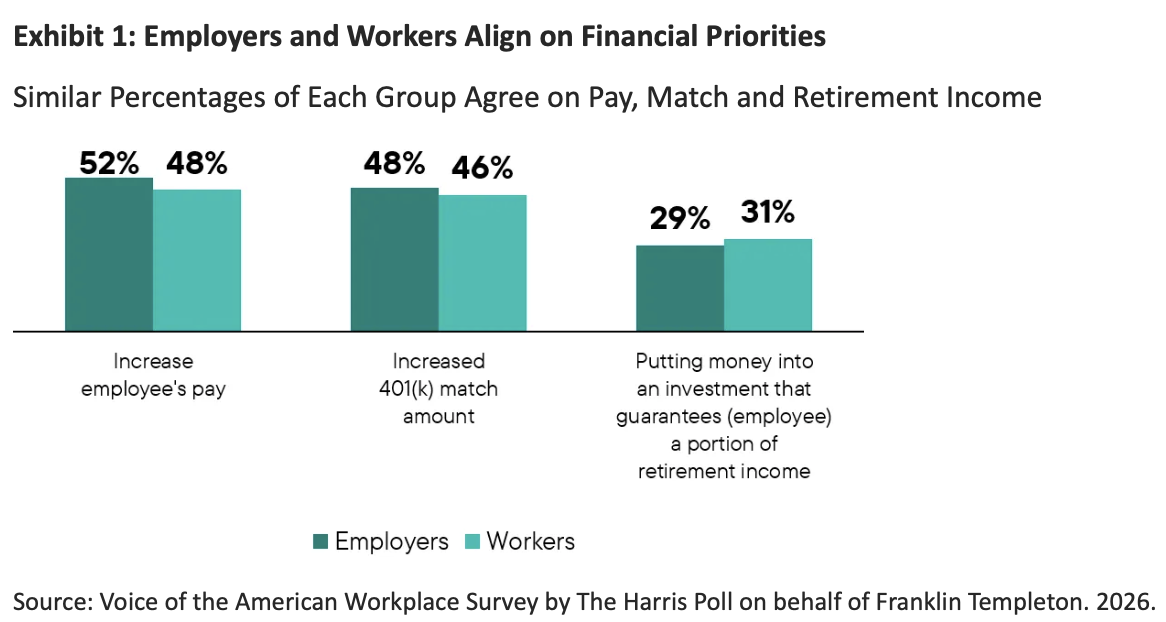

Employers and employees are not misaligned with retirement readiness. In fact, they’re remarkably aligned on what matters most:

- Competitive pay

- Strong 401(k) match

- Long-term financial security

At the same time, 93% of employers say retirement planning is a shared responsibility, not a handoff. And employees are signaling they’re open to that partnership—many rely on employer programs to guide financial decisions and value proactive support. This alignment creates the opportunity for defined contribution advisors to reinforce what is working well.

From information delivery to outcome design

The tension is clear:

- 81% of workers say benefits communication is effective

- Yet more than half still feel overwhelmed and unsure what to do next

At the same time:

- 88% want benefits explained in plain language

- 73% of employers say employees ask the same questions repeatedly

This is not a lack of effort; it is a translation gap. Participants are not asking for more information. They want clearer direction: what to do next, how to improve, and where they stand. The real market dynamic is the combination of financial stress and openness to support.

Bottom Line:

Workers are under real financial pressure: 80% turn to their employer for help with financial concerns as retirement timelines lengthen and financial milestones move further out. At the same time, engagement remains strong, with 91% wanting to learn more about their financial benefits. Many also say they might not be saving at all without features such as auto-enrollment. Together, this pressure and openness create a compelling communication opportunity for employers and their advisors.

Access the full findings here: Voice of the American Workplace Survey | Franklin Templeton

---

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

---

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

The allocation of assets among different strategies, asset classes and investments may not prove beneficial or produce the desired results.

Equity securities are subject to price fluctuation and possible loss of principal.

Funds that invest in bonds are subject to certain risks including interest-rate risk, credit risk, and inflation risk. As interest rates rise, the prices of bonds fall. Long-term bonds are more exposed to interest-rate risk than short-term bonds. Unlike bonds, bond funds have ongoing fees and expenses.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.