Who isn’t covered by a retirement plan?

Background:

New AARP fact sheets show that about half of American private sector working adults lack access to a pension or payroll deduction workplace retirement savings plan. Using methodology developed by former Federal Reserve expert John Sabelhaus and published by the Wharton School of the University of Pennsylvania, the fact sheets (national and by state) have demographic data both nationally and for all 50 states and the District of Columbia.

Findings:

About 56 million private sector workers are not covered by a retirement plan. This includes almost 78% of workers in firms with less than 10 employees, and 64% of those employed by firms with between 10 to 24 employees. In addition, over one-third of employees at companies with over 1,000 workers do not have access to a workplace retirement savings plan. Further, over 44 million workers who have annual earnings of

$53,000 or less – and another 12 million workers with earnings more than $53,000 – cannot save for retirement through a workplace plan.

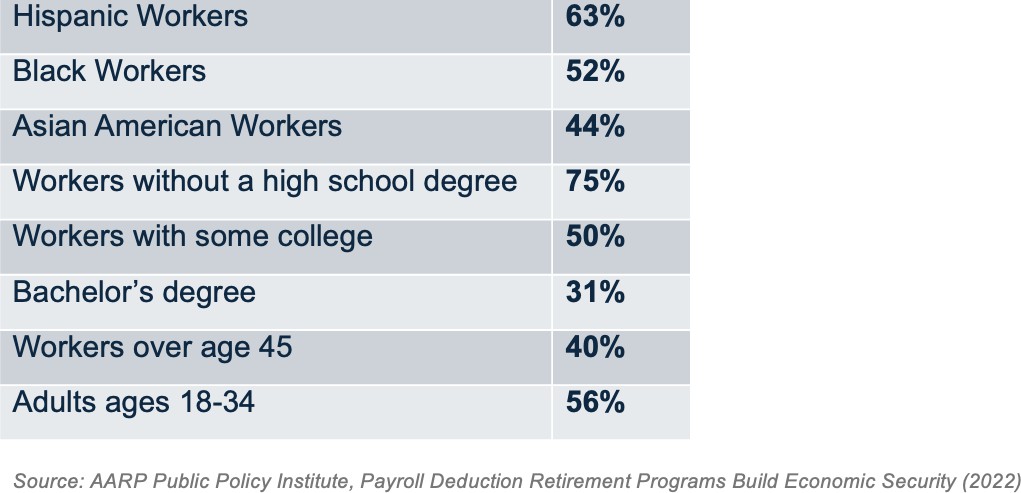

The retirement coverage gap is also higher among younger, less educated, Hispanic, and Black workers. Nearly 63% of Hispanic workers, 52% of Black workers, and 44% of Asian American workers lack access to a workplace retirement plan.

In addition, three out of four workers with less than a high school degree, 50% of workers with some college and 31% of those with a bachelor's degree do not have access to a retirement savings plan.

Finally, close to 40% of workers over age 45 and nearly 56% of adults between ages 18 to 34 lack access to a workplace plan.

The state-based fact sheets show that access to a workplace retirement savings program differs across individual states. Depending on the state, between 31% and 60% of its workers lack the ability to save for retirement at work. Florida has the highest proportion of its workforce without a pension or retirement savings program, while the District of Columbia has the lowest.

Bottom Line:

The retirement security for roughly 56 million workers can be improved by increasing access to payroll deduction retirement savings accounts. Doing so would especially benefit low-to-moderate income workers and employees of small- and mid-sized businesses.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Guest Contributors: Gary Koenig, David John, and Manita Rao. Gary Koenig is interim SVP and David John and Manita Rao are Senior Policy Advisors at AARP’s Public Policy Institute.