When participants retire, do they stay in-plan— or take their 401(k) money and run?

Background:

As seen in J.P. Morgan’s Retirement by the Numbers study, plan sponsors and investment committees can benefit from evaluating how participant behaviors interact with plan design—for both the default investment in the years leading into retirement and in the withdrawal decisions participants make once they stop working.

Findings:

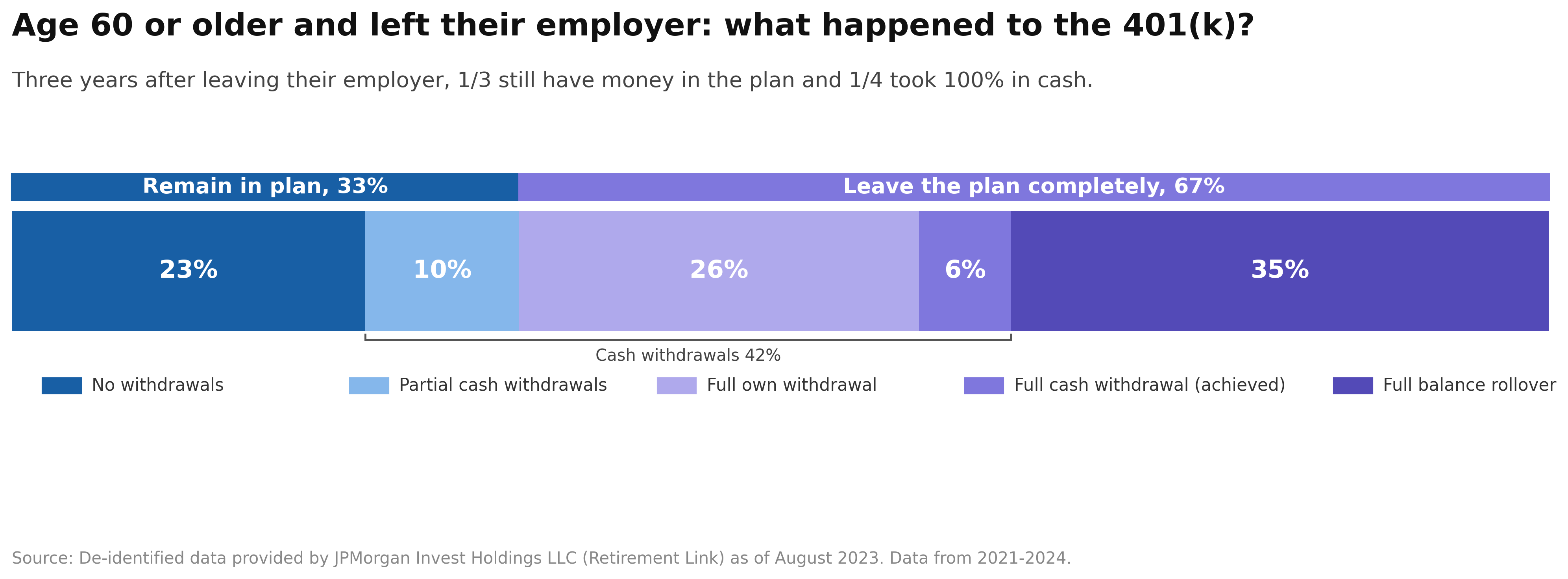

Takeaway #1: Most participants take money out—often as cash rather than direct rollovers. Within three years of leaving their employer at age 60+, 67% of participants leave the plan completely. The analysis shows that 35% complete a full balance rollover, while 26% take a full cash withdrawal and 6% take a combination of full cash withdrawal and direct rollover—meaning 42% have some form of cash withdrawal in this window.

Takeaway #2: Those who stay in-plan often wait until RMDs drive action. Among the 33% who remain in-plan, 23% take no action and 10% take partial cash withdrawals. For those still in-plan, annual cash-withdrawal activity shows a pronounced jump around the RMD starting age, and the pattern shifts in a way that aligns with the move in RMD age from 72 to 73.

Bottom Line:

For plan sponsors, two implications stand out. First, it is reasonable to expect that a significant share of participant balances will come out of the plan around retirement—and a meaningful portion may be distributed as cash withdrawals, not rollovers. Cash withdrawals that are not rolled over may not always be reinvested; if not needed for immediate spending, taking a lump sum can create sequence of return risk, reinvestment risk and the potential loss of tax-advantaged status if not reinvested in a timely manner. This should be taken into consideration when designing a default glidepath. Second, for participants who keep assets in the plan, many appear to delay withdrawals until required minimum distributions (RMDs) begin—suggesting plan sponsors have an opportunity to better support the “in-plan” retiree with clearer drawdown guidance and retirement income options before distributions become mandatory. Separately, J.P. Morgan Plan Participant Research (2024) indicates retirees value solution features such as protecting balances in down markets, income growth potential, and flexibility—signaling that retirement income design needs to balance security with adaptability.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Sources: J.P. Morgan Asset Management, Retirement by the Numbers; J.P. Morgan Asset Management, Defined Contribution Plan Participant Survey Findings.