What makes the retirement trajectories of DINK households different?

Background:

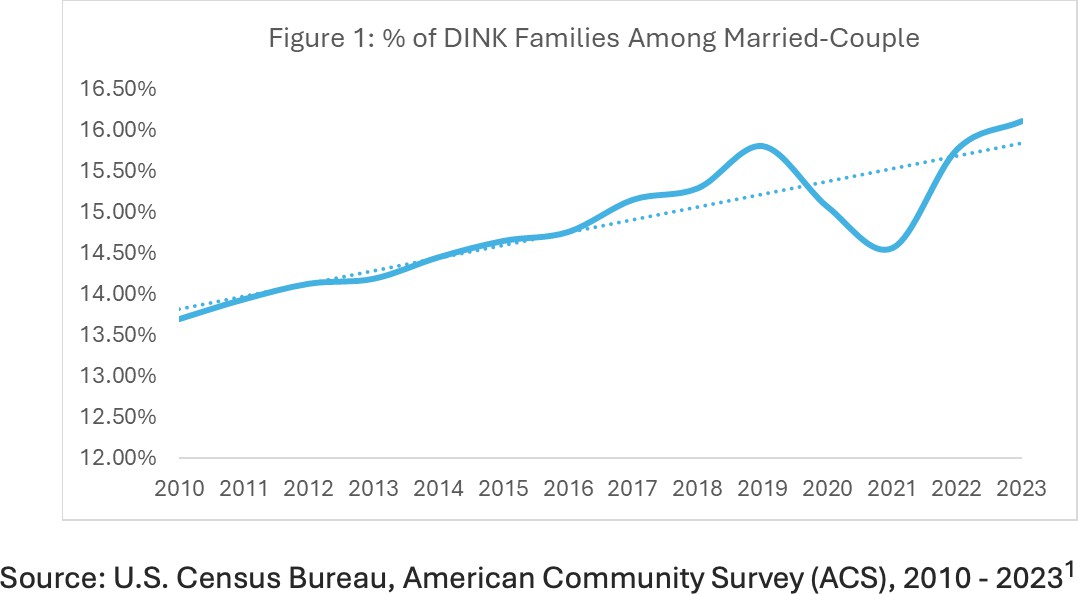

The structure of the American family has evolved significantly in recent decades, reflecting a growing diversity of family arrangements. One increasingly common structure is the dual-income, no-kids (DINK) household (as illustrated in Figure 1). Over 73% of U.S. adults now report being comfortable with a child-free lifestyle, citing financial considerations as one of the top primary factors.

According to the U.S. Department of Agriculture's Expenditures on Children by Families, 2015 report, the average cost of raising a child from birth to age 18 was approximately $233,610, excluding college expenses—a figure likely higher today due to inflation. This significant financial burden prompts an important question: does the absence of childcare costs enable DINK families to save more effectively for retirement, and how do their retirement trajectories differ from those of traditional dual-income families with children (DIWK)?

Findings:

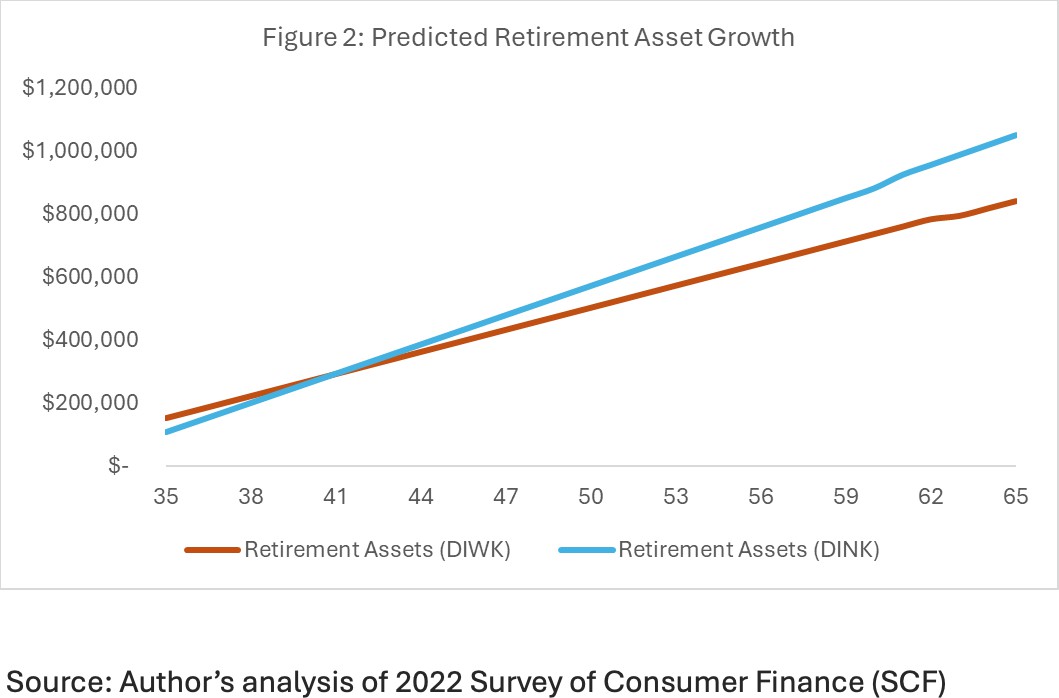

This research explores the retirement savings behaviors of DINK and DIWK families using data from the 2022 Survey of Consumer Finance (SCF). Despite having higher disposable incomes, DINK families contribute less to employer-sponsored retirement plans in their early years. However, their retirement savings accelerate significantly after mid-career, surpassing DIWK families and ultimately resulting in an average asset gap of $200,000 in favor of DINK households by age 65. (The predicted retirement assets include both workplace retirement accounts and Individual Retirement Accounts (IRAs) and is predicted after regression analysis.)

This trend highlights notable lifestyle differences. DINK families often prioritize investing in themselves, dedicating more resources to personal hobbies and interests. This lifestyle tends to emphasize present enjoyment over long-term planning, particularly in the early stages of their careers. For instance, a recent Harris Poll report revealed that DINK families spend significantly more than the average American household on discretionary purchases such as dining out, travel, and entertainment. However, as retirement approaches, DINK families demonstrate a remarkable ability to shift focus, redirecting their resources toward building substantial savings without the financial obligations of raising children.

Bottom Line:

The rise of DINK households serves as a timely reminder of the evolving dynamics within American society. For the retirement industry, the first step is to understand the unique financial behaviors of DINK families and develop tailored strategies that encourage early and consistent retirement savings. Equally critical is addressing how, without the support of adult children, these households can effectively transform their savings into sustainable income to ensure financial security in later life.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.