What influences decision-making: How can we value financial decision-making?

Background:

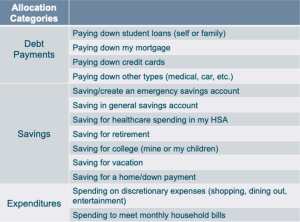

As part of the ongoing DCIIA RRC project, “Examining Employees’ Perceptions of their Next Best Dollar,” 2,500 survey participants were asked to allocate a hypothetical windfall bonus equivalent to one month’s employment income among 14 options, each of which belonged to one of the following groupings:

We then embarked on a valuation exercise for allocations made by participants to weigh how their choices may have affected their future wealth. To do this, we constructed the Future Value Index (FVI), by assigning rates of return for each savings choice, as well as interest rates for each debt payment choice consistent with current rates of return on each type of investment or loan. The maximum horizon assigned for future value was 10 years, roughly equivalent to the retirement horizon of the survey population of median age (Generation X, aged between 43 and 58 at time of collection).

Findings:

Overall, participants did well – they achieved an FVI of 1.18 on average, which means that the average future value of their bonus in 10 years’ time was 18% higher than the original value of the bonus. Roughly half of our survey respondents achieved modest gains of up to 50% over the ten-year horizon. Furthermore, 17% of respondents achieved even better gains and only 5% doubled their bonus or more over ten years.

Bottom Line:

The preliminary results show that, faced with allocating a windfall bonus, workers made decisions that, on average, enhanced their future wealth by a modest amount. However, this modest amount is less than the maximum they may have achieved by allocating to the longest-term, highest-return savings vehicle. Households often have multiple financial objectives and do not solely focus on investing for the long run.

Indeed, financial planning, in the absence of adequate consideration of each household’s financial situation and objectives, may actually prove detrimental to the household’s longer-term financial outlook. It is, however, important to recognize that improving financial literacy and promoting financial wellness can have a positive impact on long-term wealth for households with diverse financial priorities, ranging from long term savings to addressing short-term expenses.

Employers may take note of the importance of helping employees focus their financial planning not only on pure return considerations of their investments but also encouraging robust education to make informed choices to support their financial wellness.