What influences decision-making: findings from a structural equation model

Background:

The RRC recently finalized the study, “Examining Employees’ Perceptions on Their Next Best Dollar,” with the goal of better guiding employers and service providers in designing and deploying financial wellness programs for their workforce.

The RRC fielded an employee survey to 2,500 workers in February 2023, where workers were assessed on their financial literacy, household balance sheets, and engagement preferences. Notably, survey respondents also participated in a simulation exercise, where they were asked to spend a financial windfall commensurate to one month’s household wages. They were asked to allocate these dollars across options that include consumption, savings, and debt repayment.

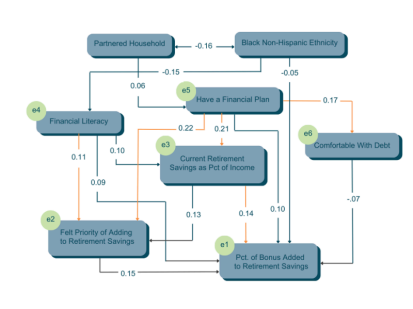

As part three of this financial wellness series, a unique analysis using a structural equation model (SEM) revealed the most compelling influences on worker’s financial decision-making.

Findings:

Over 50% of all windfall allocations were towards savings. Retirement savings and emergency savings were nearly identical, indicating competing priorities. Further, workers with higher household incomes (over $100,000) were more likely to allocate more of their windfall bonus to retirement savings, while workers with lower household incomes (below $100,000) were more likely to allocate their bonus to emergency savings.

An advanced regression analysis using a SEM was leveraged to identify the most influential variables on workers’ windfall allocation decisions. The SEM revealed that some of the top influences included:

- Financial literacy levels

- Comfort with debt (women were notably highly debt-averse)

- Marital status

- Current retirement savings balances (meaning those with current balances were more likely to save in higher proportions)

- Prioritization of adding to retirement savings (older workers felt less financially secure and more compelled to save in higher proportions)

Bottom Line:

The SEM was able to trace a pattern of positive savings behavior that adhered to the following path:

1. Workers with higher financial literacy levels were more likely to have a financial plan.

2. Those with a financial plan, either with short-term and/or long-term plan(s), were more likely to save for retirement.

3. Those who had begun saving were more motivated (i.e., possessed a Felt priority) to continue saving and to increase the proportion of savings compared to their household incomes.

The SEM also revealed two key nuances based on the variable regressions:

Younger generations in unpartnered households were less likely to have high financial literacy levels, a financial plan, nor had they begun saving. These workers were also auto-enrolled in higher proportions.

Ethnicity, as a factor by itself, did not influence decision-making related to financial priorities. This indicates a movement towards more life-stage centric or generationally centric communications.

Stay tuned for our next Journal of Retirement Guest Column, which will reveal the most financially optimal windfall decisions made and which worker groups are falling behind.