Part two: What do windfalls tell us about personal financial wellness: are there differences by gender?

This is part two of a series on financial wellness decision-making.

Background:

The RRC launched the study, “Examining Employees’ Perceptions of Their Next Best Dollar” to better understand the intersection of financial knowledge, engagement, and influences on optimal financial outcomes for workers.

The RRC fielded an in-depth, 2,500-employee survey in February 2023 to assess their financial wellness and related topics. Survey respondents participated in a simulation exercise where they were asked to spend a financial windfall equivalent to one month’s household wages. They were asked to allocate these windfall dollars across options that included discretionary spending, savings, and debt repayment.

Findings:

Distinct differences in priorities and confidence are seen between genders. As has been consistently reported elsewhere, while women have lower confidence scores (66% of men ranking high or very high levels of confidence, compared to only 34% of women), their financial literacy scores are nearly identical to men’s financial literacy scores (51% for men versus 49% for women).

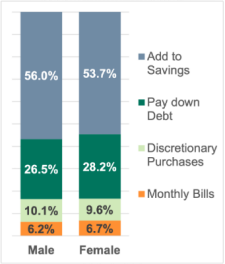

Last week’s Research Minute on this study highlighted spending priorities. When broken down by gender, responses revealed notable differences between men and women (see chart below).

Bottom Line:

These research findings indicate that men tend to allocate more of their “windfall” to savings and discretionary spending, while women are more inclined to prioritize bill payments and debt reduction. This difference is likely the result of gender pay gaps, which is confirmed by comparing allocation patterns based on household income. These gender differences highlight the challenge employers and service providers face in designing effective financial solutions, products, and financial wellness programs.

Please see our latest Guest Column in the Journal of Retirement, which provides additional details surrounding Phase One of this analysis.