What could be the evolution of defaults and emerging solutions?

Background:

In a recently published report, “Choice and Evolution in Defaults,” a working group from the DCIIA Investment Policy & Design Committee noted four key themes that guide both the optimal choice of a default today, and their future evolution:

1. Participant objectives and outcomes through accumulation and decumulation phases

2. Ease of use for participants

3. Personalization at the plan and individual level

4. Cost under continued downward pressure

Using these themes, the report reviews the current QDIA landscape to review changing participant objectives for traditional solution types as well as emerging QDIA options. An Action Kit offers related questions for consideration by plan sponsors, advisors, and other service providers.

Findings:

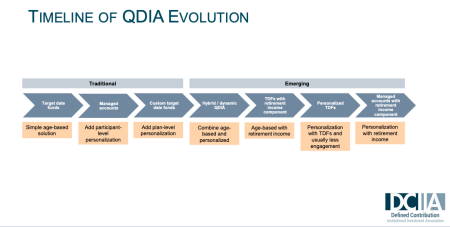

Traditional QDIAs (TDFs, plan-level cTDFs, managed accounts) favor accumulation and managed investing with limited participant engagement and low-cost options. Yet, these solutions generally have lower levels of personalization due to few data elements needed to operate. The traditional QDIAs commonly do not factor in participant-populated data, including outside assets, risk preferences, expenses, and more.

However, with more employers wanting to keep participants in-plan after retirement/termination, plans are evolving to serve as retirement income sources rather than solely focusing on retirement savings. In response, emerging default options aim to bridge that gap.

Emerging QDIA options (hybrid/dynamic, TDFs with retirement income component, personalized TDFs) favor managed investing and benefit spending to allow greater participant customization. Yet, there is limited record of adoption and utilization of these solutions due to higher costs and a higher need for participant engagement to provide additional data elements, including annuity preferences, health risks, non-traditional investments, and more.

Bottom Line:

As the fundamental purposes of DC plans continue to evolve, default solutions are also evolving. This may be a good time for plan sponsors and service providers to ask key questions such as:

- How important is it for the QDIA to focus on: accumulation? Managed investing? Managed spending/retirement income/benefit payments?

- Is the current QDIA being used appropriately by participants? How retirement ready are participants?

- What does our baseline glidepath look like, in terms of overall conservativeness / aggressiveness and shape, compared with TDF industry consensus and dispersion?

- How much, and in what ways, does our participant(s) differ from typical in terms of plan demographics, investment views, and other factors?

The full report is available here.