What are the portfolio efficiency implications of including ESG funds in a DC plan?

Background:

This piece summarizes some recently released research that I co authored with Zhikun Liu, a senior research associate at EBRI. The research focuses on the portfolio efficiency implications of including ESG funds in a DC plan by looking at the allocation decisions of 9,324 newly enrolled DC participants, across 108 DC plans, who are self-directing their accounts in a DC plan that offers at least one ESG fund.

This is part two of the Research Minute series about this study. (See last week’s Research Minute, “Do new DC participants allocate to ESG funds when available in the core menu?”)

Findings:

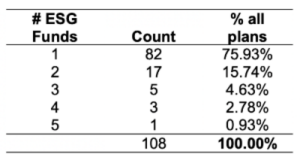

One issue with simply adding ESG funds to the core menu is that it may entice some participants to opt out of some type of professionally managed portfolio, such as a target date fund or a retirement managed account, and instead self-direct their account. DC plans that offer ESG funds tend to offer relatively few of them, as depicted in the table below, and based on the 108 plans included in our study.

Therefore, do-it-yourself (DIY) participants (i.e., self-directors) would generally need to build relatively undiversified portfolios if they want an “all ESG” portfolio or they would need to combine the ESG funds with non-ESG funds to build a well-diversified portfolio. DIY participants who allocate to ESG funds exhibit different traits than participants who do not allocate to ESG funds. For example, ESG participants tend to invest more aggressively, which is likely due to the fact that most ESG funds are equity funds.

When looking at the expected return of participants who build their portfolios, we find that the expected returns are approximately 100 basis points lower than those of investors using professionally managed portfolios such as target date funds and managed accounts.

Bottom Line:

These findings suggest that adding ESG funds to core menus has the potential to create additional implicit return “costs” for participants to the extent that the decision to allocate to an ESG fund drives participants away from professionally managed multi-asset options (e.g., target date funds).

----

Note from the RRC: Do you have data showing a similar or different take on the subject of ESG funds in DC plans? Join the discussion on LinkedIn to share your insights. RRC members are welcome to reach out about being a future guest contributor to the Research Minute - contact rrc@dciia.org.