To what extent can the Saver’s Match improve retirement outcomes?

Background:

The Saver’s Match, introduced under the Secure 2.0 Act of 2022, will provide a 50% government match on the first $2,000 of eligible retirement contributions. Using the Morningstar Model of US Retirement Outcomes, we analyzed the program’s potential impact on retirement wealth for a representative sample of Generation Z and Millennial workers under four behavioral scenarios, which reflect eligible individuals starting to save or saving more to get the full match. The simulation accounts for realistic behaviors, including cashouts and pre-retirement withdrawals, with higher rates applied to lower-income individuals with smaller account balances.

Findings:

The analysis reveals that the Saver’s Match could significantly boost retirement savings, particularly for historically disadvantaged groups and workers in lower-income industries.

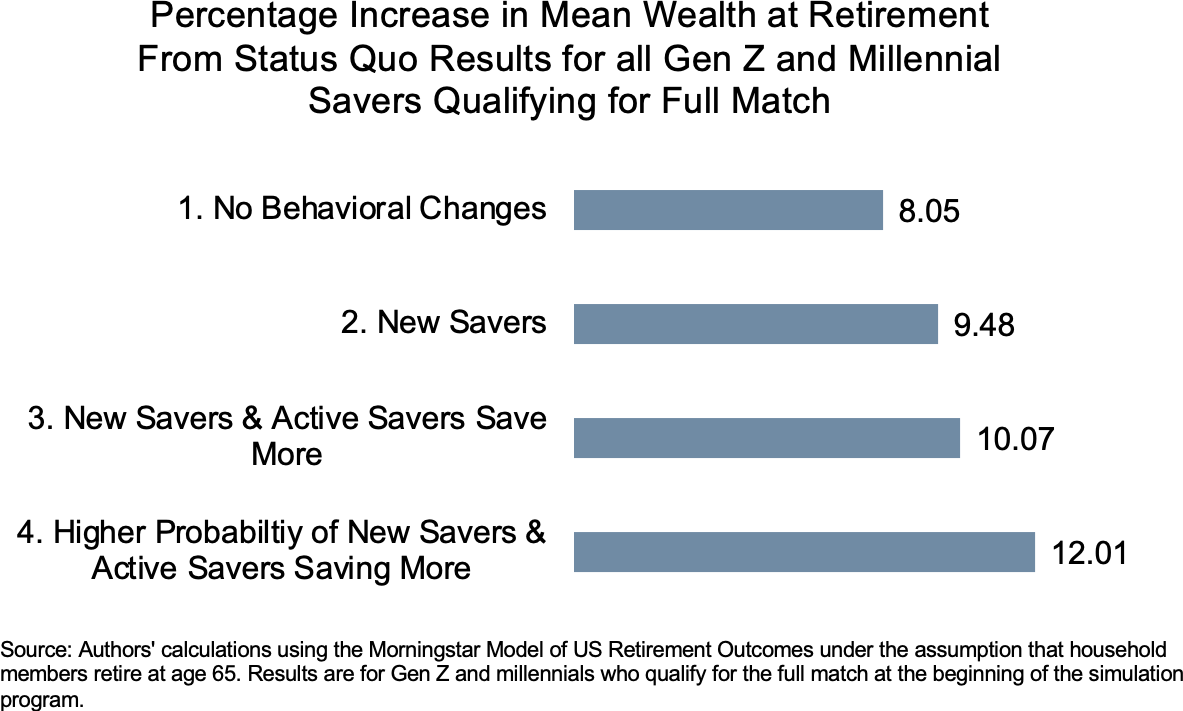

Overall Impact: Eligible savers could see mean retirement wealth increases of up to 12.01%. Even in the most conservative behavioral scenario, where no changes in saving habits occur, participants still experienced a mean retirement wealth increase of 8.05%.

Single Women: Eligible single women are projected to benefit more than men and married couples, with a greater proportion of single women qualifying for the match. Moreover, single women often see a larger percentage increase in wealth at retirement than other groups, with potential retirement wealth increases of up to 13.13%.

Black and Hispanic Americans: Similar to single women, Black and Hispanic Americans are more likely to qualify for the match, with 48.9% of Hispanics and 3.5% of non-Hispanic Black Americans meeting the eligibility criteria compared to just 28.7% of non-Hispanic white Americans. Furthermore, Black and Hispanic Americans see larger projected gains than other demographic groups with mean wealth increases of up to 14.57% and 12.10%, respectively.

Industry Variations: Workers in industries with higher retirement-income inadequacy, such as agriculture, mining, and construction, and wholesale and retail trade stand to benefit the most.

Behavioral Response is Key: Intuitively, the greatest increases occur when individuals actively adjust their savings to maximize the match. Plan sponsors, in particular, can make a big difference by providing targeted communication aimed at low- to moderate-income workers who might qualify.

Bottom line:

The Saver’s Match has the potential to meaningfully improve retirement outcomes, particularly for lower-income and underrepresented groups. However, its success will depend on effective implementation and outreach, ensuring that eligible individuals understand and take full advantage of the program.

-----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.