Through a DEI Lens: Where are the disparities and how can they be addressed? Part Three

How much could "treatment" of pre-retirement withdrawals help to mitigate gender and race/ethnicity differentials in defined contribution plan outcomes?

Background:

In part one of this “Research Minute” series, I looked at the ratio of account balances to salary by age, gender and race/ethnicity for a synthetic universe of defined contribution participants.In part two of the series, I focused on the disparities in pre-retirement withdrawals for these groups. In the final part of this series, I provide some preliminary evidence on how much "treatment" of pre-retirement withdrawals could help to mitigate gender and race/ethnicity differentials in defined contribution plan outcomes.

Findings:

The data for this analysis comes from the Collaborative for Equitable Retirement Savings (CFERS). As confidentiality is of paramount importance in this project, I created a synthetic universe for this analysis. Each plan in the synthetic universe is equally weighted to mask the results for the larger plans. While this is still based on actual data (year end 2021), the results cannot be reverse engineered to see plan-specific results. This will be replaced with unweighted data once the sample size is sufficiently large.

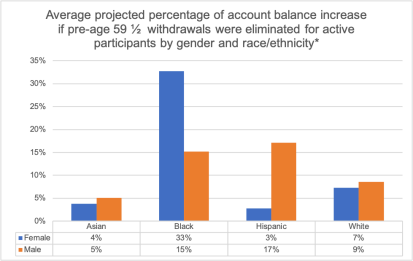

Projected account balances at age 65 were derived for all active participants currently ages 35-39. Age-specific average results for contributions, loan activity, probability of pre-retirement withdrawals and average percentage of account balance taken out in a pre-retirement withdrawal were used for each of the eight combinations of gender and race/ethnicity seen in Figure 1. For the purposes of this preliminary analysis, deterministic rates of return of 6% per year and salary growth of 3% per year were assumed. After the baseline account balance for each participant was projected, the process was repeated assuming no pre-retirement withdrawals were taken. The projected percentage of account balance increase was computed for each participant and the averages were broken out by gender and race/ethnicity in Figure 1.

Although all groups of participants have an average increase if pre-retirement withdrawals are assumed not to occur, there is a significant difference among the groups. Those groups who are less likely to take a pre-retirement withdrawal (see part two for details) would have a relatively smaller impact to their balances. By comparison, Black males are projected to have a 15% increase in account balance whereas Black females (whose annual probability of a preretirement withdrawal in this sample is 85% above average) are projected to have a 33% increase.* Synthetic universe. The sample is limited to participants currently ages 35-39 and filters out participants with a salary of less than $10,000.

Bottom Line:

Although the findings in this three-part series are currently limited to exploratory analysis and projections on an early version of the CFERS data, it shows the potential power of demonstrating existing disparities, analyzing what is causing them and the degree to which changing participant behavior through plan design modifications as well as educational campaigns are likely to mitigate these differentials. As the sample size increases, we look forward to working with each plan sponsor in the database to explore which modifications are most likely to achieve their particular objectives in mitigating these differentials.

If you are interested in participating or would like additional information, please contact me at: jack.vanderhei@morningstar.com.