Through a DEI Lens: Where are the disparities and how can they be addressed? Part One

How does the ratio of defined contribution (DC) plan account balances to salary vary by gender and race/ethnicity categories

Background:

Based on simulation work that I published last year, it would appear that U.S. families currently between the ages of 35 and 64 will experience retirement deficits that vary drastically by race and ethnicity. Under the baseline assumptions, families headed by Black workers would have an average retirement deficit approximately two thirds greater than families headed by white workers, while families headed by Hispanic workers were expected to have an average retirement deficit approximately one half greater than families headed by white workers. Another study published in 2019 shows the impact of gender and family status on retirement deficits, with single females on the verge of retirement having a deficit more than one and a half times greater than single males.

While several studies have documented the disparities in current DC plan account balances by gender and race/ethnicity, it would be useful to determine what is causing these differences as well as quantifying how helpful various plan design modifications would be in mitigating the disparities.

In part one of this “Research Minute” series, we look at the ratio of account balances to salary by age, gender and race/ethnicity for a synthetic universe. Part two will look at gender and race/ethnicity differences in various components that drive the account balances (contributions, asset allocation, loan activity and pre-retirement withdrawals). Part three will use this information to investigate how treatment of pre-retirement withdrawals would help to mitigate the disparities seen in part one.

Findings:

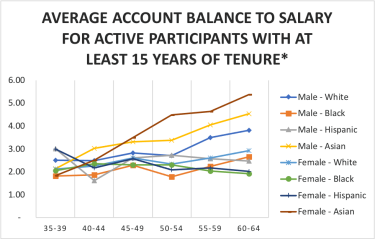

The data for this analysis comes from the Collaborative for Equitable Retirement Savings. We use the ratio of account balance to salary to control for differences in salary and further limit the sample to participants with at least 15 years of tenure with the current employer.

While the relative rankings of gender and race/ethnicity combinations vary by age in Figure 1, overall it appears that Asian females have the best outcomes, with an average differential relative to age cohort mean of positive 30%. Asian males have the second best outcome, with an average differential of positive 20%. White males also have a positive average differential of 6%.

Black males appear to have the worst outcomes from this synthetic universe, with an average differential relative to age cohort mean of negative 25% followed closely by Black females with an average differential of negative 21%. Hispanic females have an average differential of negative 14% while Hispanic males have an average differential of negative 9%. White females have an average differential of negative 11%.* Synthetic universe. The sample filters out participants with a salary of less than $10,000.

Bottom Line:

DCIIA, the Aspen Institute Financial Security Program and the Morningstar Center for Retirement and Policy Studies have launched this joint initiative (CFERS) to analyze anonymized DC plan participant data to understand differences in how participants from different demographic groups use, experience, and benefit from their retirement plans. This data will provide the basis for analysis designed to assist plan sponsors to take specific actions within the DC system to help mitigate existing disparities.

If you are interested in participating or would like additional information, please contact me at: jack.vanderhei@morningstar.com.