Retiree Perspectives: Part 4: How do pension plans impact retiree income?

Background:

In late 2021, the Retirement Research Center (RRC) surveyed over 2,000 retired workers to gauge attitudes about savings, spending, and financial wellness in retirement. This is Part 4 of the RRC’s Research Minute about this study. Among those with a defined contribution plan balance, these retirees were separated into two groups —those “With Pensions” and those “Without Pensions.” (Those without pensions have zero percent of their income resulting from a pension, from themselves or their spouse).

Findings:

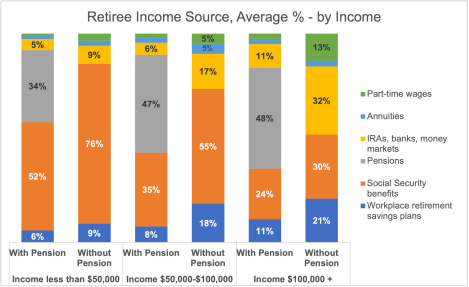

When comparing these groups, we found that across retirees With Pensions, pension income makes up 44% of their income and Social Security 37%, on average. Those Without Pensions are much more reliant on Social Security, providing 61% of income, on average.

When assessing both groups, we found significant disparities across income levels (see chart). For those Without Pensions that have incomes of less than $50,000 per year, Social Security provides three-quarters of retirement income, which is substantially higher than those With Pensions.

Among retirees With Pensions with mid-range income levels ($50,000-$100,000) and high incomes ($100,000 or more), pension income makes up the largest share of retiree income, at just under half. For those in the same income groups Without Pensions, pension income is relatively offset by income from IRAs, bank accounts, and workplace retirement savings plans.

Bottom Line:

This analysis highlights the large influence of pensions as compared to other sources of retirement income, and, when evaluated by income level, this impact is more substantial. As a growing portion of future retirees’ income is derived from non pension sources, retirement income products and withdrawal strategies will become increasingly important.

See last week’s Research Minute, “Part 3: What influences expected vs. actual retirement ages?”