Retiree Perspectives: Part 3: What influences expected vs. actual retirement ages?

Background:

In late 2021, the Retirement Research Center (RRC) surveyed over 2,000 retired workers to gauge attitudes about savings, spending, and financial wellness in retirement. This is part 3 of the RRC’s Research Minute about this study. (See last week’s Research Minute, “How do marital status and gender impact retiree spending attitudes?”). This retiree research report series will be published later this summer.

Findings:

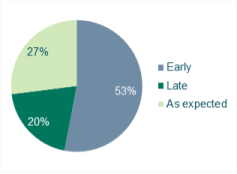

More than half of respondents (see chart) said they retired earlier than expected with just over a quarter reporting that they retired as expected. One in five retirees indicated retiring later than expected, on average working 4 years longer. For those who retired earlier than expected, they did so, on average, 5 ½ years early. Women are somewhat more likely to retire earlier than expected (55% of women versus 51% of men). Similarly, unmarried retirees of both genders were also more likely to retire earlier than expected, with 63% of single retirees reporting that they retired sooner than expected as compared to 51% of married respondents.

Retirement age is also impacted significantly by health, as those who retired at their expected retirement age or later were more likely to report good or excellent health as compared to individuals who retired early.

Bottom line:

Based on these findings, individuals who are single, women, and/or in relatively poorer health are more likely to retire earlier than expected. Retiring earlier leads to fewer accumulation years, relatively higher retirement plan withdrawals, and could potentially strain financial security in retirement.

In Part 4 of Retiree Perspectives, we will explore the influence of pension income.