Is personalization the next chapter for target date solutions?

Background:

Target date strategies have become the primary investment vehicle for U.S. employees in defined contribution plans. Designated by regulators as acceptable qualified default investment alternatives (QDIAs), these diversified strategies automatically adjust portfolio risk based on a set retirement date, making them a prevalent choice for retirement savers. However, the growing interest in personalization—evident in the increasing adoption of managed accounts—suggests that tailored investment solutions could further enhance retirement outcomes, particularly as participants near retirement.

Findings:

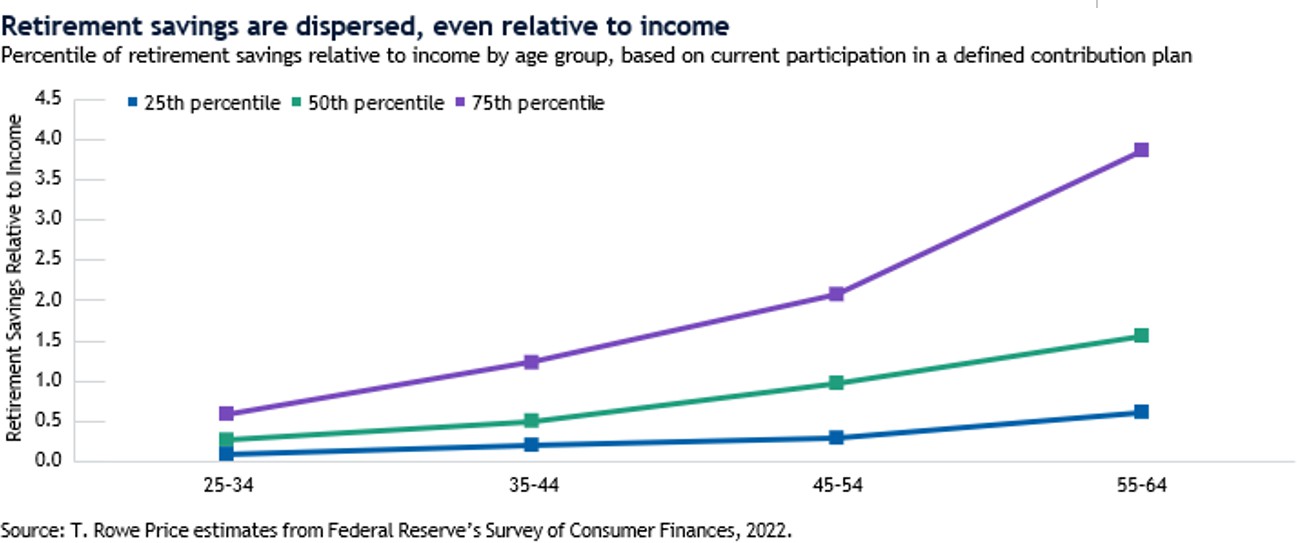

Personalization is seen as the next evolution in target date solutions. While target date strategies have supported more successful outcomes for retirement savers, data show that, as participants age, disparities in retirement savings within age groups are evident. For instance, analysis of the Federal Reserve’s Survey of Consumer Finances showed stark differences in savings within the same age groups, even after accounting for income.

This demonstrates that factors other than income contribute to savings disparities. This diversity in financial circumstances shows a need for personalized strategies to address varying retirement preparation needs. By leveraging advancements in technology, the personalization of target date solutions is now more feasible and cost-effective than before.

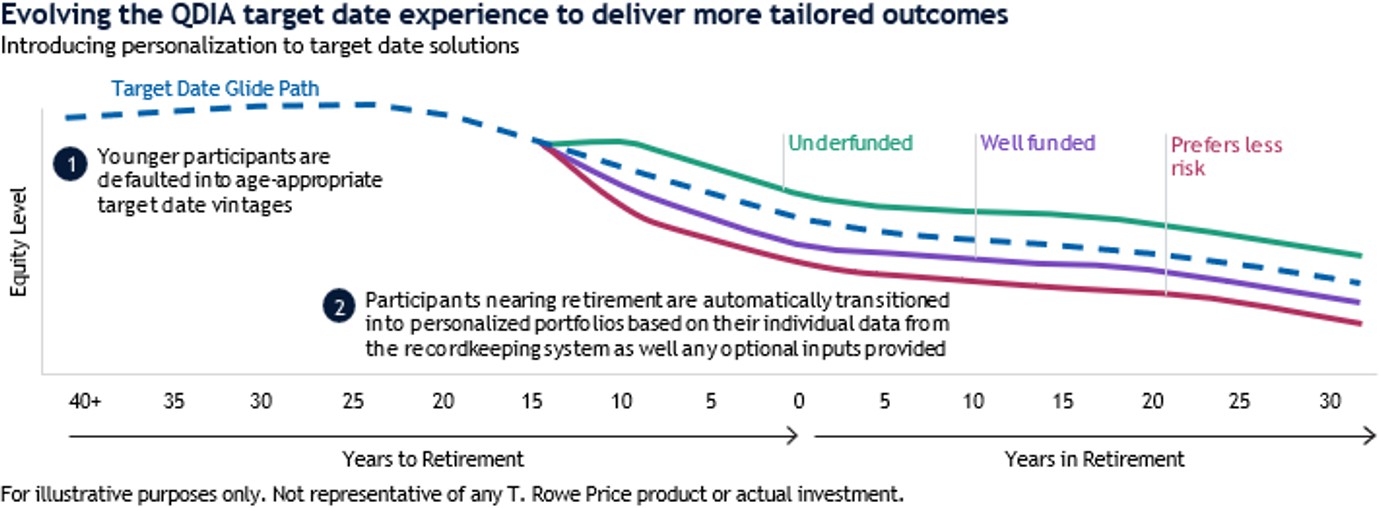

Integrating individual and demographic financial data—such as marital status, income, debt-to-income ratios, and net worth—into target date strategies could better align them with personal financial realities and help generate improved risk-adjusted outcomes. We advocate for a “target date AND personalization” approach rather than seeing these as mutually exclusive options.

By integrating personalization into the existing target date framework, plan sponsors can enhance the retirement experience for participants nearing retirement without requiring a shift to different investment methodologies or building blocks.

Bottom Line:

Introducing personalization into target date solutions could considerably improve retirement outcomes. The ability to tailor investments using available recordkeeping data and optional participant-provided information can make personalization accessible and beneficial without imposing significant engagement burdens. Maintaining a consistent investment methodology and using the same investment building blocks across both target date and personalized solutions are critical to ensuring a coherent participant experience. Personalized strategies can be achieved through a dynamic QDIA structure—one that automatically transitions participants into tailored portfolios as they near retirement—or as an opt-in service.

Target date solutions have significantly advanced the U.S. retirement landscape, and personalization represents a promising frontier. Leveraging technology and data integration can enable more nuanced and effective retirement savings strategies, potentially offering the best of both worlds. It no longer needs to be target date solutions or personalization—it can be both!

----

Guest Contributors: Sudipto Banerjee, Ph.D., Director of Retirement Thought Leadership, T. Rowe Price; Jessica Sclafani, CAIA,Vice President, Global Retirement Strategist, T. Rowe Price

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Important Information

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action. The views contained herein are as of September 2024 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types; advice of any kind; or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc., distributor, and T. Rowe Price Associates, Inc., investment adviser.© 2024 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.