Is ‘longevity literacy’ the key to better retirement readiness?

Background:

Longevity literacy is an understanding of how long people tend to live in retirement. While such knowledge enables and promotes appropriate retirement planning and saving, it is nonetheless an under-the-radar issue.

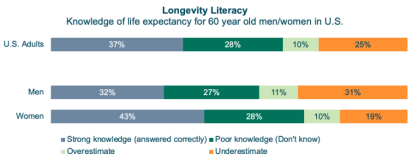

The TIAA Institute GFLEC Personal Finance Index has gauged longevity literacy for the first time with a question asking life expectancy at age 60. Response options included the correct answer (age 82 for men; age 85 for women), overestimate and underestimate responses, and a “don’t know” option.

Findings:

More than one-half of U.S. adults either underestimate life expectancy at age 60 (25%) or respond, “don’t know” (28%); 37% answer correctly. While financial literacy levels among women tend to lag that of men, the opposite is true regarding longevity literacy – the share of women who answer correctly exceeds that of men by 11 percentage points. Analogously, the share of men underestimating life expectancy at 60 is 12 percentage points greater.

Poor longevity literacy matters because longevity literacy is associated with retirement readiness. Those with better longevity literacy more typically plan and save for retirement and retirees with better longevity literacy tend to experience better financial outcomes.

Bottom line:

Longevity literacy is an overlooked factor in addressing retirement preparedness. Individuals without a realistic understanding of life expectancy in retirement are missing one of the most foundational components of any plan: a time horizon. Improving people’s longevity literacy can enable and promote better retirement readiness.

Read the full report here.

Please write to surya.kolluri@tiaa.org or PYakoboski@tiaa.org with any questions.

----

Guest contributors: Surya Kolluri is the head of the TIAA Institute. Paul Yakoboski is a senior economist with the TIAA Institute.

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. RRC members are welcome to reach out about being a future guest contributor to the Research Minute - contact rrc@dciia.org.