How can we improve annuity literacy across diverse knowledge spectrums? (Part One)

Background:

The newly released 2024 OASDI Trustee Report indicates that the projected depletion date for the trust fund remains 2033, which is only nine years away. With increasing uncertainty surrounding future Social Security retirement income, providing guaranteed lifetime income (GLI) for defined contribution (DC) plan participants has become a top priority for the retirement industry. However, understanding the benefits and potential risks associated with GLI solutions—often provided through underlying annuities—can be challenging for participants who lack sufficient knowledge and familiarity with annuity products.

In this study, we investigated whether DC participants' general financial knowledge, including both their self-assessed knowledge levels and objective test scores, affects their comprehension of annuity products. Additionally, we examined whether working with a financial advisor strengthens or weakens this impact. This is part one of a two-part series.

Findings:

Between March and April 2023, we surveyed over 1,300 current DC participants, on a set of nine basic and advanced annuity knowledge test questions. We performed a series of linear regression models to examine the association between general financial knowledge and annuity literacy, as well as the effect of financial advisors. Here are some of the key findings:

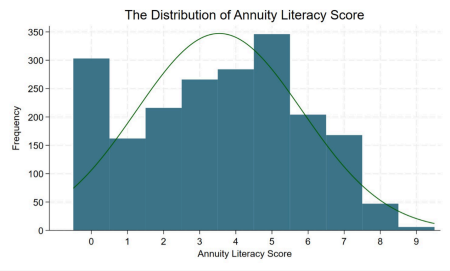

1. While the majority demonstrated a certain level of annuity knowledge, a significant proportion (14%) could not answer a single question correctly (shown in Figure 1).

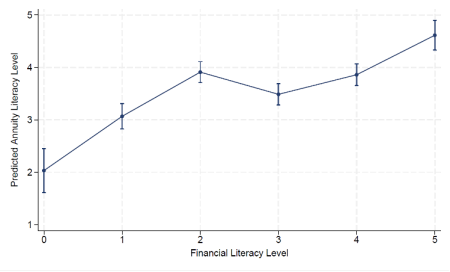

2. In general, financial knowledge enhances participants' understanding of annuities, and the limitations of using annuities to fund retirement income (shown in Figure 2).

Bottom line:

A large portion of DC participants are lacking basic knowledge about annuity products. This lack of understanding regarding the underlying products of GLI solutions can lead to a lack of confidence in making critical retirement income decisions. Although this study found that higher basic financial knowledge helps improve participants' annuity literacy, other factors can influence this relationship.

In the next Research Minute, we will delve into these complexities and emphasize the need for plan sponsors to tailor their communication strategies about the benefits of guaranteed lifetime income solutions based on participants' varying levels of financial knowledge.

----

*Source: Korankye, T., Sun, Q., & Pandey, S. (2024). The Role of Financial Advisors in Promoting Annuity Literacy: Insights into the Moderating Effect of Financial Knowledge – working paper.

**Source: Author's calculation based on data from Korankye, T., Sun, Q., & Pandey, S. (2024). The Role of Financial Advisors in Promoting Annuity Literacy: Insights into the Moderating Effect of Financial Knowledge. The predicted result is the marginal effect of an ordinary least squared model, controlling for individuals' social demographic and financial factors.

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.