How can employers and service providers best support caregivers' ability to save for their children’s education?

Background:

The DCIIA RRC and Commonwealth recently published a joint study on how parenting and caregiving expenses are influencing individuals earning low to moderate incomes (LMI) and their ability to save for emergencies and retirement. This research was designed to understand the direct links between caregiving expenses, emergency savings, retirement savings behavior, and the ability to save for a child’s future education needs. Just over 1,000 individuals were surveyed, with 66% LMI and 34% non-LMI full-time workers who have access to a retirement plan but may or may not participate.

Findings:

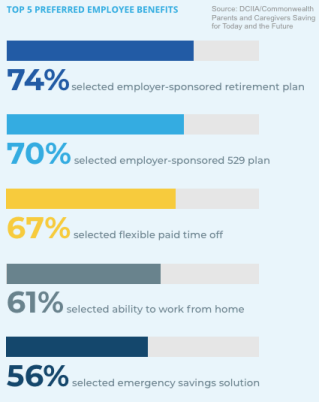

This research found that employer-sponsored 529 plans may be a feasible tool to build long-term college savings for caregivers earning LMI, if paired with an emergency savings solution and supported with financial education. In this survey, the majority of LMI workers (70%) reported that their second preferred employee benefit was an employer-sponsored 529 plan, which trailed an employer-sponsored retirement plan.

Respondents selected liquidity and portability as the most important features of an employer-sponsored 529 account, with the ability to access funds in case of emergency as the most popular choice. This was more predominant among Black caregivers (48%) as compared to white caregivers (37%).

Bottom line:

These findings suggest that employers may want to consider offering a 529 plan alongside an emergency savings option. By incorporating a liquid emergency savings “sidecar,” employers can address workers' immediate financial needs while aiding them in saving for their children's future education expenses. Additionally, employers and recordkeepers may want to explore the possibility of delivering comprehensive education on 529 plans to retirement plan participants, with a particular focus on tailored assistance for LMI workers.