Does the retirement math still work?

Background:

Goldman Sachs Asset Management's 2025 Retirement Survey & Insights Report, based on 5,102 Americans, introduces the "new economics of retirement." It highlights how rising costs and competing financial priorities are reshaping retirement planning, making affordability a central concern for savers nationwide. In this Research Minute, we will explore these evolving realities, the feasibility of retirement readiness, and potential solutions.

Findings:

Retirement planning historically relied on a simple formula: save steadily, invest wisely, and let time do the rest. However, Goldman Sachs Asset Management suggests that it is under strain. Rising costs, stagnant wage growth, and expanding financial obligations are fundamentally reshaping how Americans perceive and prepare for retirement.

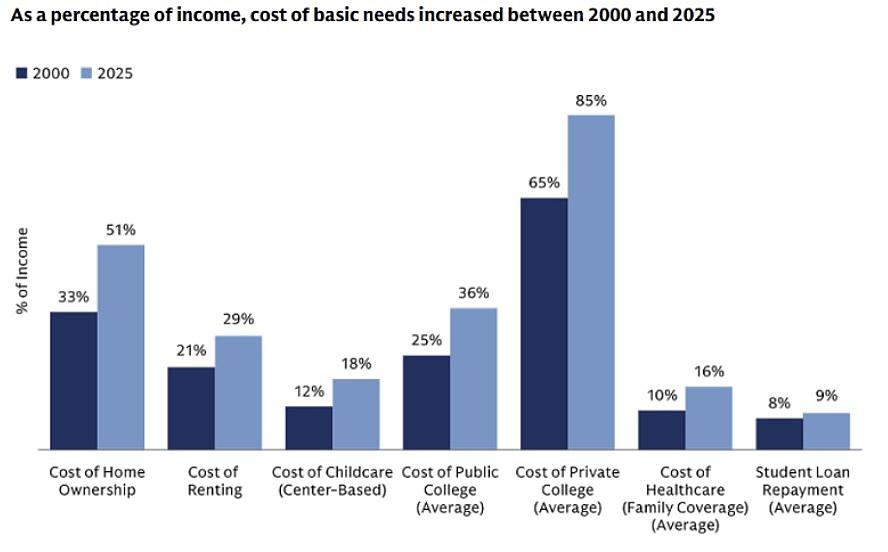

The report highlights a key paradox: 68% of savers feel on track, yet nearly 60% worry their savings won't last, showing fragile confidence. This insecurity stems from escalating basic living costs, described as a Financial Vortex. Since 2000, housing, healthcare, childcare, and education have outpaced wage growth, consuming income and limiting households’ ability to save. For example, homeownership costs rose from 33% of income in 2000 to 51% in 2025, private college from 65% to 85%, and healthcare from 10% to 16%.

This burden disproportionately impacts younger generations. The report found that 42% of Gen Z, Millennial, and Gen X workers live paycheck-to-paycheck, with nearly three-quarters (74%) of those living paycheck-to-paycheck struggling to save for retirement due to competing financial priorities. In contrast, Baby Boomers are twice as likely to characterize their financial standing as 'considerably better,' indicating a perceived ability to achieve both short-term and long-term financial objectives.

Consumer research shows this trend is growing. If it continues, 55% of workers may be living paycheck-to-paycheck by 2033 and 65% by 2043, making retirement saving increasingly difficult.

So, does the retirement math still work? Not in the way it once did. The old assumptions – that steady saving alone would secure a comfortable retirement – are increasingly outdated. Today's environment demands new thinking, flexible planning, and policy innovation.

Emerging solutions include new early savings accounts, personalized advice, protected lifetime income, diversified private market investments, and developing Financial Grit. These strategies help manage risk, support growth, and tailor planning to individual goals.

Bottom Line:

“Save more” is no longer enough. Modern retirement planning must reflect today’s economic realities. With thoughtful plan design, innovation, and personalized guidance, retirement readiness remains possible. The retirement landscape and math may have changed, but with the right solutions, retirement readiness can still be within reach.

Read the full report here.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.