Does annuitized income lead to better financial well-being?

Background:

As employer-sponsored retirement plans shifted from DB plans to DC plans, the annuitization rate inside Americans’ retirement portfolios vastly decreased. Without data, it is hard to identify how this change impacts a household's financial well being. By exploring data from the 2016 and 2020 Health and Retirement Studies (HRS), this summary presents empirical evidence on whether annuitized income increases households' financial well-being in three dimensions: economic hardships, objective financial ratios, and subjective financial strains, and how the effect changed before and after the COVID-19 pandemic.

Findings:

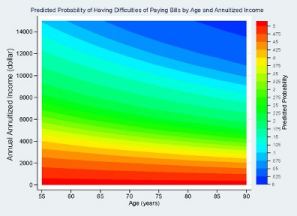

Results from models indicate that annuitized income significantly reduces the difficulties of paying bills, eases financial strains, and improves financial ratios. For example, the marginal effects in Figure 1 show that when Americans increase their annual annuitized income from $0 to $14,000 (the median amount from the HRS sample), they reduce the chance of experiencing difficulties paying bills from 50% to below 15%.

Figure 1:

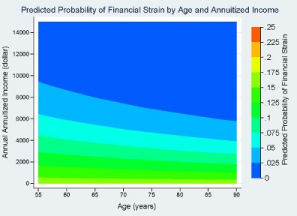

In Figure 2, this positive effect is even more significant for older retirees, who could reduce the chance of experiencing difficulties to almost zero. In terms of subjective financial strains, the effect of annuitized income is more extensive. For retirees between ages 55 to 90 years old, an increase of $10,000 in annual annuitized income will ease financial pressures (reduce the chance of financial strains to zero).

Figure 2:

Bottom line:

It's critical to help DC plan participants realize the importance of diversifying their retirement income resources. They may consider making up the portion of their annuitized income that previously came from DB plans by replacing bond assets with annuitized assets around retirement age. This understanding could assist plan sponsors as they consider introducing access to lifetime income options.

From the author’s publication, “Sustaining Retirement During Lockdown: Annuitized Income and Financial Well-Being Before and During the COVID-19 Pandemic".