Does advisor-type influence Social Security claiming age?

Background:

Delayed claiming of Social Security retirement benefits is a widely touted strategy to improve retirement income outcomes. In theory, households working with financial advisors should be more likely to exploit this opportunity, since financial advisors have expertise in helping clients achieve their financial goals, and households that use financial advisors have higher life expectancies.

In recent research published in the Retirement Management Journal, we explore how advisor compensation is related to Social Security retirement benefit claiming decisions using data from the 2019 Survey of Consumer Finances. It focuses on three general compensation models: hourly (i.e., accountants), assets under management (i.e., financial planners), or commission (i.e., brokers and bankers).

Findings:

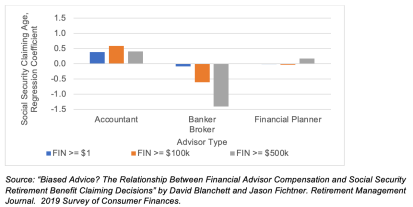

The key results are highlighted in the graphic below, which includes the difference in claiming ages by advice-type when controlling for a variety of demographic factors when households are grouped by the total amount of financial assets (FIN). A positive coefficient means the household using that type of advisor claims later than households without any kind of financial advisor, on average, and vice versa.

We find there are notable differences in Social Security claiming age by advisor-type. For example, households with higher levels of financial wealth, who generally have the most discretion around when to claim benefits, who were working with an advisor paid hourly (i.e., accountants) claimed benefits two years later than households working with a commission-based advisor (i.e., brokers). This is somewhat surprising.

Bottom line:

The results suggest compensation methods may impact the quality of financial advice received by households and may bias advisors against certain strategies. The fact that households working with any type of financial advisor do not uniformly claim Social Security retirement benefits at later ages, regardless of compensation method, and that some households using certain types of advisors claim at younger ages, is a bit surprising given how widely the benefits of delayed claiming are covered in the financial press.

Overall, our research suggests that financial advisor compensation has the potential to impact recommendations and that more research on this effect is warranted.

----

Guest contributors: David Blanchett, head of retirement research and portfolio manager, PGIM DC Solutions; Jason Fichtner, chiefeconomist, Bipartisan Policy Center; executive director, Retirement Income Institute, Alliance for Lifetime Income