Do we have retirement fluency in the U.S.?

Background:

For the first time, the 2024 TIAA Institute-GFLEC Personal Finance Index (P-Fin Index) assessed retirement fluency in addition to financial literacy among U.S. adults. What is retirement fluency? Simply put, knowledge that promotes financial well being in retirement. This research highlights another dimension of the retirement income security challenge confronting Americans.

Findings:

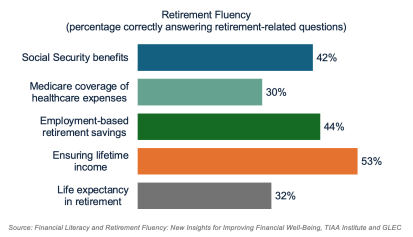

Five questions covering five distinct subjects were used to gauge retirement fluency: Social Security benefits, Medicare coverage of healthcare expenses, employment-based retirement savings, ensuring lifetime income, and life expectancy in retirement. Respondents correctly answered two questions, on average, and struggled most with the questions about Medicare coverage and life expectancy. Only 30% of U.S. adults have a general understanding of Medicare’s average coverage rate of health care expenses in retirement. Only 32% know how long people tend to live upon reaching retirement age. On the other hand, slightly more than half of all respondents (53%) know that annuities provide lifetime income.

Furthermore, retirement fluency can be linked to retirement readiness. Twenty-six percent of those who correctly answered four or five of the retirement fluency questions are very confident they will have enough money to live comfortably throughout retirement, while only 7% are not at all confident. These figures are essentially flipped among those who did not correctly answer any of the questions (10% and 29%, respectively).

Bottom line:

Initiatives to improve retirement fluency are not a panacea for poor retirement income security, but clearly matter in concert with efforts to address other challenges in the retirement ecosystem, such as retirement plan coverage gaps in the workplace. Future research will build out a more robust view of retirement fluency.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.