Do new DC participants allocate to ESG funds when available in the core menu?

Background:

There is limited research on the actual allocation decisions DC participants make to ESG funds. This piece summarizes some recently released research, which I co-authored with Zhikun Liu, EBRI. This research explored the allocation decisions of 9,324 newly enrolled DC participants, across 108 DC plans, who are self-directing their accounts in a DC plan that offers at least one ESG fund.

Findings:

Among DIY investors, allocations to ESG funds are relatively modest when offered in the core menu. Only 8.9% of participants had any allocation to an ESG fund and the average allocation to ESG funds among those who hold at least one ESG fund was 18.7% of the total balance. The average allocation to ESG funds among all the DIY participants included in the analysis, as a percentage of the total DC balance, was only 1.7%.One potential driver of the relatively low ESG fund allocations is the limited number of ESG funds offered in core menus. For example, among plans that offer ESG funds, 76% only offered one ESG fund, which was most commonly an equity fund (77% of funds), with Large Blend being the most common investment style (51% of all ESG funds available).

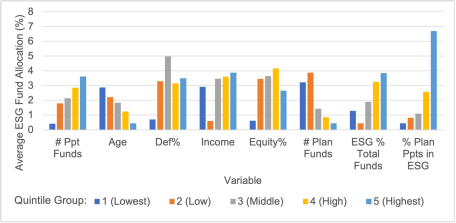

The table below provides some context as to how average ESG allocations (as a percentage of the total balance) varied across different attribute quintile groups. The legend under the chart indicates quintiles with 1 being the lowest and 5 is the highest. The precise breakpoints are included in Appendix 1 in the main paper.

The two factors which appeared to drive the largest allocations to ESG funds were not related to participant demographics:

1. The number of funds participants held in their portfolio. The decision to allocate to the ESG fund is a weak preference and not necessarily a signal of conviction in ESG.

2. The percentage of participants in the respective DC plan allocating to an ESG fund. The more new participants in the plan that had an allocation to ESG funds, the higher the average fund allocation tended to be. This suggests plan interest effects could be an especially strong driver of future growth in ESG funds (despite relatively low usage today).

Bottom Line:

Overall, this research suggests demand for ESG funds among DC participants may be significantly lower than suggested by a number of surveys on the topic and that plan sponsors should take a thoughtful approach before adding ESG funds to an existing core menu.

Do you have data showing a similar or different take on the subject of ESG and participant engagement? Join the discussion on LinkedIn to share your insights. RRC members are welcome to reach out about being a future guest contributor to the Research Minute - contact rrc@dciia.org.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC.