Do Managed Accounts Improve Retirement Outcomes in Defined Contribution Plans?

Guest Contributor: Jack VanDerhei, Director of Retirement Studies, Morningstar Center for Retirement and Policy Studies

Background:

Managed accounts (MAs) are a growing feature in defined-contribution plans, offering personalized investment allocation and savings guidance. Adoption has increased as plan sponsors seek to improve participant outcomes through more tailored solutions. However, debate remains about whether MAs provide incremental value beyond existing plan features such as target-date funds (TDFs) and automatic enrollment with escalation. This study uses the Morningstar Defined Contribution Outcomes Model (DCOM), a participant-level microsimulation framework, to evaluate the impact of MAs on projected retirement wealth while controlling for demographics and plan design features.

Findings:

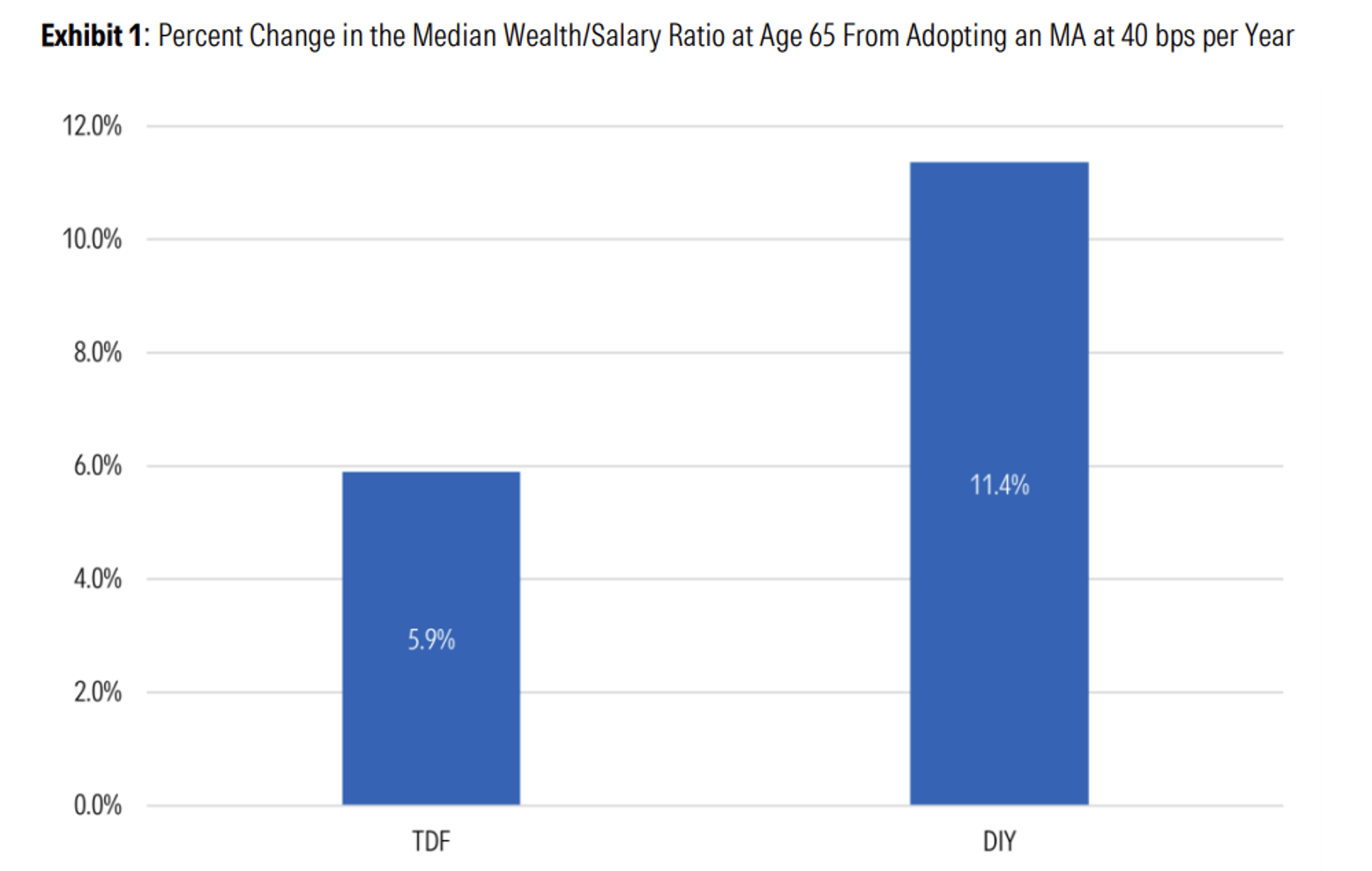

The analysis shows that managed accounts improve projected retirement outcomes across participant types and plan designs. On average, adopting an MA increases the median balance-to-salary ratio at age 65 by 7.7%, with larger gains for self-directed (DIY) investors than for target-date fund (TDF) investors. The primary driver of these improvements is higher contribution rates, suggesting that personalized savings recommendations play a larger role than asset allocation alone.

Benefits are most pronounced among younger and newer participants, reflecting the compounding effect of increased savings over time. Participants early in their careers experience materially larger gains than those closer to retirement. Similarly, participants with shorter tenure realize larger improvements due to lower starting savings rates and balances.

Lower- and middle-income participants also experience the greatest relative gains, as incremental increases in saving have a larger proportional impact on retirement wealth. Across plan designs, MAs offer positive outcomes even in plans with automatic enrollment and escalation, though the magnitude is smaller in more structured environments.

A common critique of these results is that they reflect selection bias, with more motivated participants choosing to enroll in managed accounts. However, the observed patterns are difficult to reconcile with a pure selection explanation. After controlling for age, wage, tenure, and plan design features, higher contribution rates persist among MA users. More importantly, the largest increases occur among younger, lower-income, and shorter-tenure participants—groups historically less likely to exhibit proactive savings behavior. This pattern is more consistent with a behavioral effect driven by structured savings guidance than with selection alone.

Bottom Line:

Managed accounts offer consistent, positive improvements in projected retirement outcomes, primarily by increasing participant savings behavior. Their value is greatest for younger, lower-income, and less-engaged participants, and they remain beneficial even in plans with strong automatic features. For plan sponsors, the results suggest that personalization can complement, rather than replace, existing plan design strategies.

Source: Morningstar Center for Retirement and Policy Studies. “Analyzing the Value of Managed Accounts,” 2026.

---

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

---

Disclosures

©2026 Morningstar Investment Management LLC. All Rights Reserved. The Morningstar name and logo are registered marks of Morningstar, Inc. Morningstar Retirement offers research- and technology-driven products and services to individuals, workplace retirement plans, and other industry players. Associated advisory services are provided by Morningstar Investment Management LLC, a registered investment adviser and subsidiary of Morningstar, Inc.

This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security.

The performance data shown represents past performance. Past performance does not guarantee future results. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason.