Are pre-retirees financially ready for the retirement they envision?

Background:

Voya’s Consumer Insights and Research Team conducted an in-depth research study among pre-retirees to gain a better understanding of their financial priorities and concerns, as well as their ideal visions for retirement. Pre-retirees are defined as adults aged 50-70 who are benefits-eligible, working full-time or part-time with an employer-sponsored retirement plan, and annual household income of $75k+, and investible assets of $100k+.

This research consisted of a two-phased approach:

1) 60-minute in-depth qualitative interviews among 12 pre-retirees conducted between December 17-20, 2024, through Voya’s proprietary online consumer community managed by Material. Participants in the consumer online community received compensation for participating and they were not Voya clients.

2) A 20-minute online survey among 517 pre-retirees was conducted between December 17-20, 2024, in partnership with Morning Consult.

Findings:

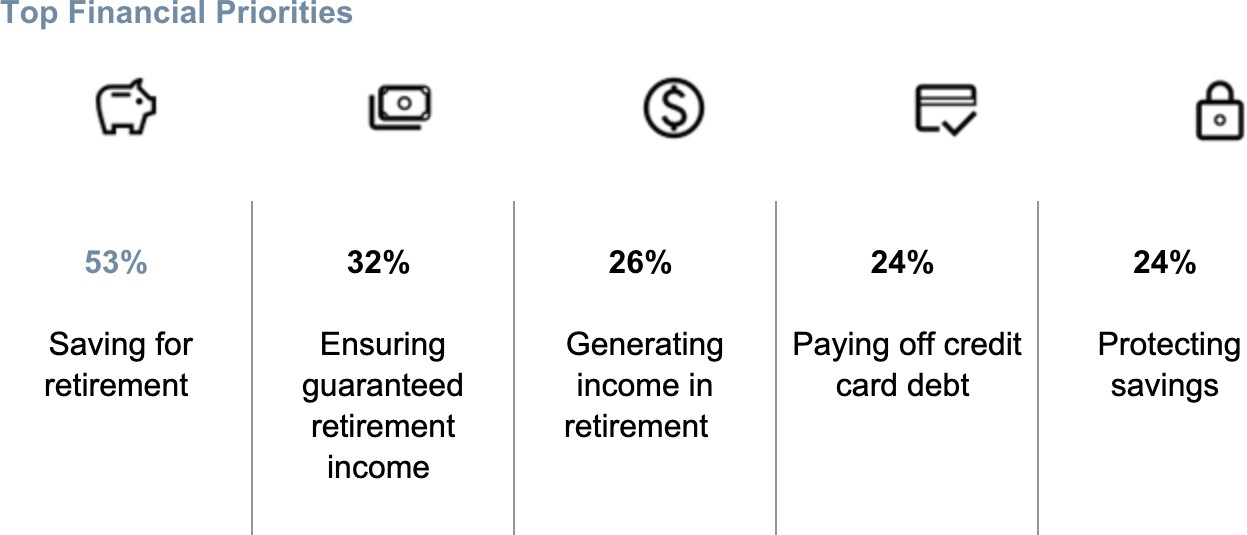

Pre–retirees demonstrate a strong savings mindset; only 46% have a formal plan for generating income in retirement. While most live comfortably within their means, 20% still live paycheck to paycheck. Their top financial priorities include saving for retirement (53%), ensuring guaranteed income (32%), and managing debt and savings protection. Concerns are dominated by inflation, market volatility, and the sustainability of Social Security benefits.

Despite 84% feeling somewhat or very prepared for retirement, only 55% believe they are likely to achieve their ideal retirement lifestyle, which typically includes travel, hobbies, and staying active. Half of pre-retirees plan to work during retirement, often to maintain purpose or supplement income. Retirement savings are diversified across Social Security, workplace plans, IRAs, and investments, with 49% likely to retain assets with their current workplace retirement plan provider. Additionally, 74% expect to leave a financial legacy, primarily to children, and 69% are interested in employer-provided estate planning support.

Bottom Line:

Personalized planning support is critical: Many pre-retirees delay formal income planning until close to retirement. Providers have an opportunity to engage earlier with tools and guidance tailored to individual financial situations.

Supporting holistic retirement readiness: While financial preparedness is high, aligning expectations with retirement lifestyle goals remains a challenge. Providers can support this by offering educational resources and planning tools that help individuals visualize and prepare for their desired retirement experience.

Workplace providers as trusted resources: Retirement plan providers are the most utilized source of information. Expanding their role to include healthcare cost estimation, income conversion strategies, and legacy planning could deepen engagement.

Flexibility and purpose in retirement: With 50% of pre-retirees planning to work post-retirement and many expressing interest in staying active, supporting phased retirement options can help individuals transition on their own terms with the flexibility to pursue purpose-driven activities.

Legacy and intergenerational wealth: The strong intent to leave a financial legacy underscores the need for accessible estate planning tools and education, especially as housing affordability and caregiving responsibilities influence family dynamics.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.