Are 401(k) millionaires financially literate?

Background:

Accredited investors are assumed to be financially sophisticated individuals and are therefore able to participate in more complex investment strategies. The latest SEC review of the accredited investor definition questions whether qualified retirement assets, which would include IRAs and 401(k)s, should be excluded from net worth when determining accredited investor status, given that “those individuals may have little, if any, prior investing experience and may not seek the assistance of professional advisors.” For this analysis, we leverage data from the Federal Reserve’s 2022 Survey of Consumer Finances (SCF) to explore how financial literacy varies among different types of investors. This is a summary of a recent study published through the DCIIA RRC.

Findings:

The SCF includes three questions to gauge financial literacy, asking about the risk of company stock, compound growth, and inflation. Known as the “Big Three,” these questions are useful when assessing how people understand basic financial concepts (Lusardi and Mitchell, 2011). To the extent financial literacy is an accurate proxy for financial sophistication, wealth appears to be a good determinant for the accredited investor definition, since financial literacy scores tend to improve by wealth levels (but not by age).

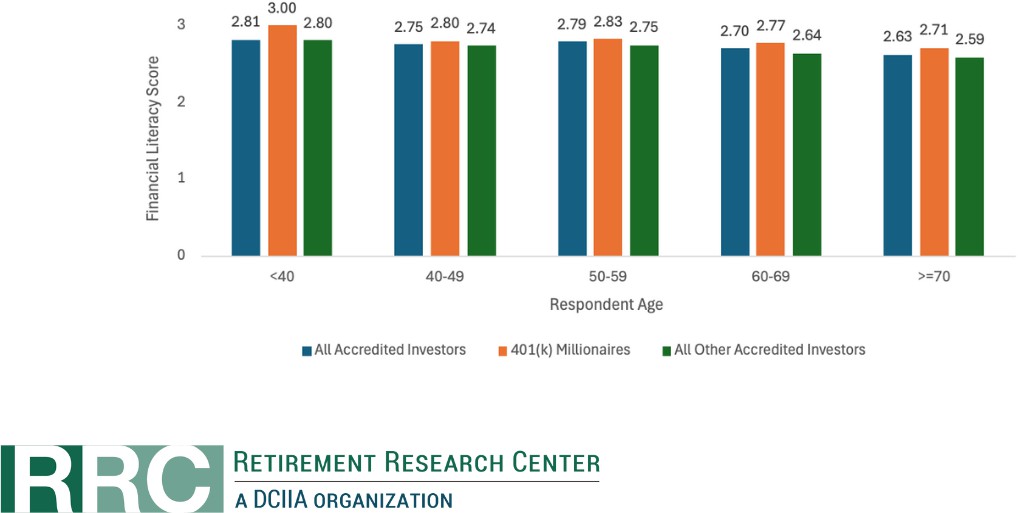

For the analysis, we separate those households that meet the accredited investor definition into those who have $1 million or more in qualified savings, who we call “401(k) millionaires,” and all other accredited investor households. The following chart includes the average number of correct responses to the three financial literacy questions in the SCF answered for the two groups, by respondent age.

We see that average financial literacy scores are higher among “401(k) millionaires.”

Additionally, 401(k) millionaires have higher levels of self-assessed knowledge on personal financial matters and tend to have more years of education compared to other accredited investors, both of which would generally be assumed to be positively related to financial sophistication.

Bottom Line:

Contrary to suggestions that qualified retirement savings should be excluded from estimates of financial sophistication, we find evidence that households with significant qualified retirement savings are more financially literate. One potential explanation for this effect is that it takes decades of good decision making to accumulate a sufficient level of savings to be a “401(k) millionaire,” even for the relatively unengaged. Therefore, suggestions that excluding qualified assets from net worth under the accredited investor definition seem counter to the actual financial sophistication levels of those investors who manage to accumulate significant levels of qualified savings.

----

Insights shared by guest contributors are their own and do not represent the views of DCIIA or the RRC. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Guest Contributors: David Blanchett, Head of Retirement Research and Portfolio Manager, PGIM; Drew Carrington, Managing Director, iCapital